Content

- Business Operations

- What Is The Expense Recognition Principle?

- Benefits Of The Matching Principle

- Why The Matching Principle Is Important For Small Businesses

- Accounting Principles 5, 6, And 7 Description

- Finance Your Business

- The Top Financial Challenges Faced By Small Business And How To Overcome Them

Matching of expenses to revenues is defined as the process of collecting all revenues which are earned during the accounting period and matching these revenues with the expenses incurred to produce those revenues. In the matching process, revenues are first recognized and expenses are then matched against these revenues.

Another benefit is a more accurate reporting of a business’ operating results because the revenues and expenses were matched at the same time. Where sales, expenses and TEP may change over time t but the expense elasticities of sales revenue are constant. The second aspect is that all expenses incurred by the business, enabling it to provide the service, should be duly accounted for in the income statement for the period in which the credit for the fee is taken.

Business Operations

However, this rank correlation between the sub-period correlations was only 0.353 referring to different types of matching behavior in the sub-periods. In 3.0 per cent of firms, the revenue-expense correlation was negative in the first sub-period and positive in the second. Similarly, in 1.8 per cent of the firms, this correlation was negative in the second sub-period and positive in the first. However, for the whole 10-year period the percent of negative correlations was only 0.5 per cent.

What is the difference between revenue recognition and realization?

As a process of recording revenue, recognition is continuous. Realization is the point when recognition ends. The former is precise and accurate, while the latter is an estimate. For companies deferring revenue, this is important for accurate forecasting.

Integrate all of your applications, from accounting to marketing to procurement, into a cohesive software environment with full transparency into all financial data. Invoices that don’t match get flagged for further review, and payment may be delayed while the AP team chases down exceptions. If you recognise an expense later than is appropriate, this results in a higher net income. For example, if you’re a roofing contractor and have completed a job for a customer, your business has earned the fees.

What Is The Expense Recognition Principle?

It becomes very difficult to track the revenue that comes because of the marketing campaign. So, the marketing expense would appear in the income statement when the ads are shown. So, what do you do with expenses that don’t have a clear cause-and-effect relationship? In a case like this, there are two classifications it could be categorized under. Otherwise, the title should have been passed onto the buyer so as to create a legal obligation for the buyer to pay for them. The second aspect is that the full cost of those items must be included in that particular period’s income statement. First, that the revenue has been earned in the period in which it is included in the income statement.

- When a business delivers a product or a service to a customer, accountants say it has made a sale.

- Furthermore, the persistence of earnings will decrease with poor matching, as it brings negative autocorrelation in the time-series of earnings.

- This important point is greatly omitted in research although REC potentially suffers from several weak points as a measure of the quality of matching.

- Compensation may impact where products are placed on our site, but editorial opinions, scores, and reviews are independent from, and never influenced by, any advertiser or partner.

- On the balance sheet at the end of 2018, a bonuses payable balance of $5 million will be credited, and retained earnings will be reduced by the same amount , so the balance sheet will continue to balance.

- Similarly, if a fee is earned for providing a service, the first test is to ensure that the service in question has been duly provided.

In practice, the matching principle combines accrual accounting with the revenue recognition principle . When businesses interpret financial statements, those statements must be calculated and prepared in a certain manner to abide by proper accounting principles.

Benefits Of The Matching Principle

Learn accounting fundamentals and how to read financial statements with CFI’s free online accounting classes. Thank you for reading this guide to understanding the accounting concept of the matching principle. And presents a more accurate picture of a company’s operations on the income statement.

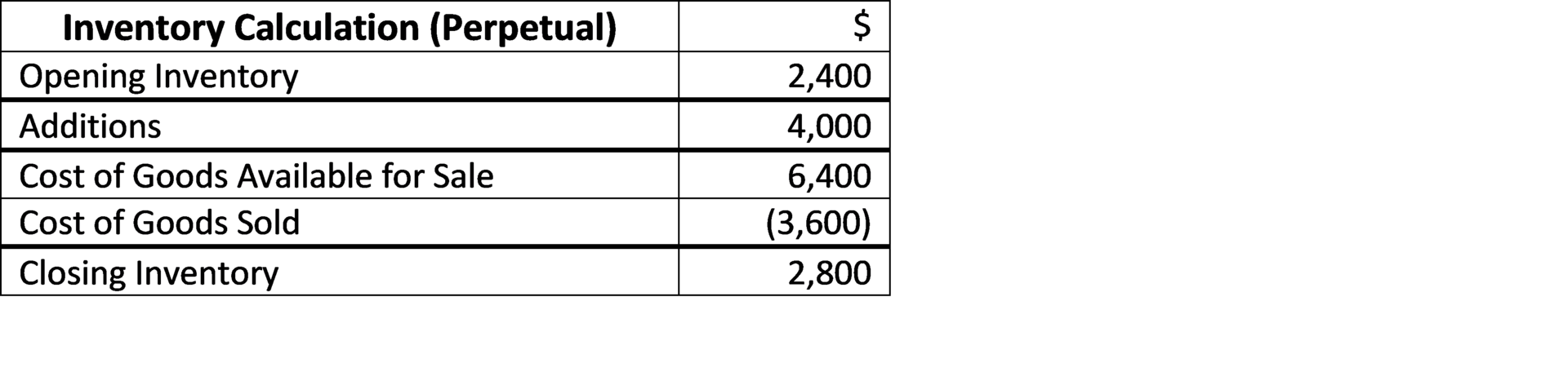

The requirement for this concept is the allocation of cost to different accounting periods so that only relevant incomes and expenses are matched. This comparison will give the net profit or loss for that particular accounting period. There are many instances in accounting in which you will need to use the matching principle. Some of those include when expenses and revenue will occur in different accounting periods, using inventory costing systems, accounting for accrued interest, and estimating future warranty claims.

Why The Matching Principle Is Important For Small Businesses

First, it introduces a general matching function concept where revenue is described by a multiplicative model of time and different expense categories. This kind of approach provides useful information about the change in efficiency in expenses over time and the sensitivity of different expense categories to matching. Secondly, the coefficient of determination of the matching function provides us with a useful measure of matching the accuracy of revenue and expenses that takes account of the change of the expense efficiency in time. This measure is also constructed to avoid the hidden mismatching bias and it is expected to give a more reliable picture of matching accuracy than the REC based measures. This approach can be used to show how these events or factors are related to the matching sensitivity of different expense categories. A company that incurs an expense that it has yet to pay for will recognize the business expense on the day the expense arises.

Second, since large and complex businesses recognize revenue and match expenses independently of cash flow, keeping track of the cash position of the company is more difficult than it would be otherwise. For a subscription SaaS provider, this can mean breaking up the money received from an annual subscription into the monthly periods as the services are provided. This provides auditors with a so-called apples-to-apples comparison of a company’s financial picture that is more transparent across industries. Expensing a portion of the cost of the conveyor belt over its useful life, you will be using the matching principle as you match any revenue earned with the expense of the asset throughout the life of the asset. However, the commission payment will not be processed until the 15th of February.

Accounting Principles 5, 6, And 7 Description

Companies can use the accrual method of accounting if their revenue is below a specific threshold set by the IRS called the gross receipts method. When this is not easily possible, then either the systematic and rational allocationmethod or the immediate allocation method can be used. The systematic and rational allocation method allocates expenses over the useful life of the product, while the immediate allocation method recognizes the entire expense when purchased. Your company bills clients at the end of the month for the services you’ve provided during the month. Most of your clients pay within the allowed time period, but some—due to issues with the payment system, a forgetful manager, the invoice hitting the spam folder, etc.—do not pay on time. Because of the matching principle, the expenses on the statement are not necessarily those things that we purchased that month, or even paid for that month.

Each dollar or unit of currency spent must have an offset, such as wages paid or items purchased for the business. Sales entries contain sales to customers matched with the inventory cost for the item sold; materials purchased for sale are matched with the spent cash; and wages paid are matched with the liability owed to employees. The accrual accounting method uses the principle as a self-balancing tool to maintain the accuracy of the general ledger.

However, over time, the organization will be able to average out a percentage of expenses that it is likely to pay over time. This concept tries to make sure that there no over or under revenue or expenses records in the financial statements. If the revenue or expenses records inconsistently, then there will be over or under revenue or expenses. If the above measurement principles are unsuitable to the matching principle expense, then the costs are expensed in the period in which they are incurred. These include costs for which there is no clear future benefit, the benefit is not certain, and costs for which no allocation method can be devised. While the IRS does not require a single method of accounting for all businesses, it does impose certain limitations that impact which accounting method a company can use.

- The $100,000, however, is not an expense used to generate revenue for the same period in year one.

- For example, rent for the office, officer salaries, and other administrative expenses.

- Therefore, to overcome this, one can segregate expenses in two different categories – period and product costs.

- If hypothesis H2 is supported by empirical evidence, it has important implications.

- It is specified as a multiplicative Cobb-Douglas-type function of three categories of expenses .

Under the matching principle, expenses are reported with revenue and not necessarily entire expenditures for the period. Accrued revenue—an asset on the balance sheet—is revenue that has been earned but for which no cash has been received. The most common include accounts payable, accounts receivable, goodwill, accrued interest earned, and accrued tax liabilities. This is a lot to take in at once, but with practice you’ll be able to quickly deduce when and where your revenue and expenses need to be reported. Good financial statements are the heart of any business, and keeping them in order is a surefire way to keep tax authorities happy.

The Top Financial Challenges Faced By Small Business And How To Overcome Them

This recurring journal entry will be made for each subsequent accounting period until the prepaid rent account has been depleted, which will be in December. However, the commissions are not due to be paid until May, so you will need to accrue the $4,050 for the month of April since the expense is clearly tied to the sales revenue that was earned in April. In order to use the matching principle properly, you will need to record a monthly depreciation expense in the amount of $450 for the next three years, or over the useful life of the equipment. By accruing the $900 in January, Jim will ensure that he is in compliance with the matching principle of reporting expenses in the same time period as sales. Designed to be used with accrual accounting, the matching principle is never used in cash accounting.

naol matching principle ha

— salve (@svlmdmb) November 26, 2021

Dichev and Tang conclude that poor matching increases the volatility of earnings because the mismatched expenses act as a noise that is not related to the economics process of creating earnings. Furthermore, the persistence of earnings will decrease with poor matching, as it brings negative autocorrelation in the time-series of earnings.

- Fourthly, in a perfect matching situation, the volatility is driven entirely by economic factors.

- If revenues and expenses are not recorded properly, both your balance sheet and your income statement will be inaccurate.

- This means that the machine will produce products for at least 10 years into the future.

- Before any invoice is paid, the accounts payable team reviews each line item to ensure the pricing, quantities, terms, and item descriptions match those on the purchase order.

- As a concept it is used in many different settings to help professionals keep track of what is going in and what is coming out, and it can help companies and businesses make sound financial decisions.

- Both of these investments will generate revenue in the long-term, but there’s no way to draw a direct line between dollars spent and future revenue generated.

Business expense categories such as prepaid expenses use the matching principle in similar fashion as depreciation. For example, in January, your business prepaid annual rent in the amount of $15,000. Revenue recognition covers the tools, procedures and guidelines a business follows to record income data. So, to extend our example, general research and development costs without direct ties to revenue created by the sale of goods and services would be charged to the related expenses account immediately.

‘Checklist of Efficiency’–OKC Earns Sixth-Best November Defense by Honing Fundamentals Oklahoma City Thunder – OKCThunder.com

‘Checklist of Efficiency’–OKC Earns Sixth-Best November Defense by Honing Fundamentals Oklahoma City Thunder.

Posted: Tue, 30 Nov 2021 17:15:00 GMT [source]

As per the policy, the employees get 5% of revenues that the company generates over the year. Therefore, it should pay its employees a bonus of $5 million in January 2019.

Paradigm shift in EU’s collaboration with HE in Africa – University World News

Paradigm shift in EU’s collaboration with HE in Africa.

Posted: Mon, 29 Nov 2021 11:49:49 GMT [source]

Author: Kim Lachance Shandro